Client Portal Login

Client Portal Login  Pay Bill

Pay Bill

The Tax Implications if Your Business Engages in Environmental Cleanup

If your company faces the need to “remediate” or clean up environmental contamination, the money you spend can be deductible on your...

If your company faces the need to “remediate” or clean up environmental contamination, the money you spend can be deductible on your...

Retail and restaurants now have a safe harbor income tax accounting method to determine whether costs paid to refresh or remodel a...

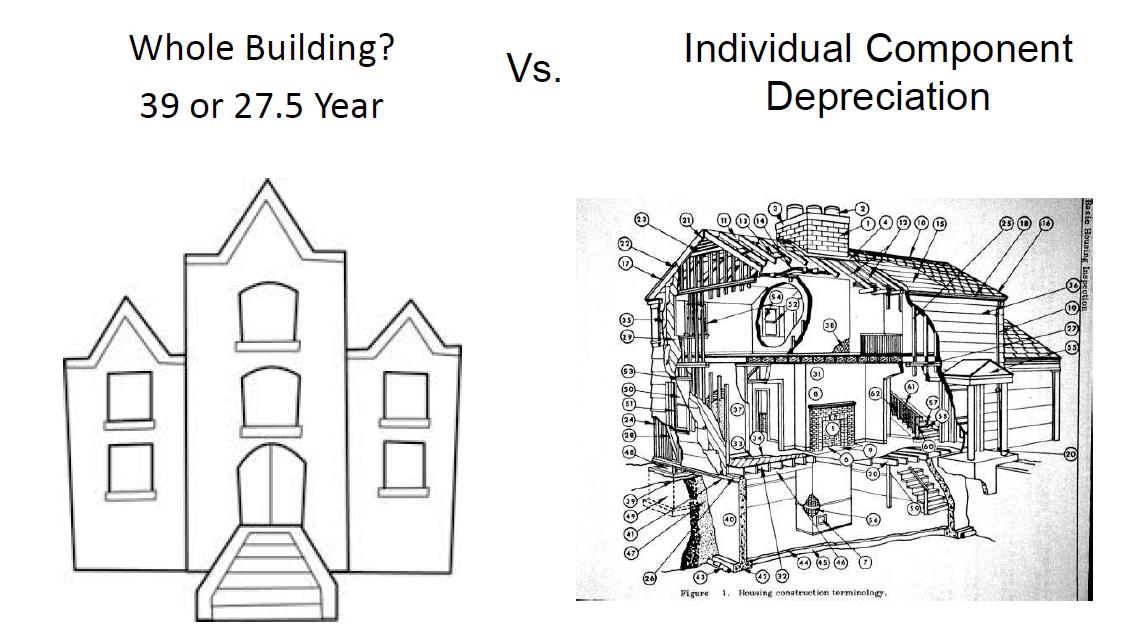

Deducting and capitalizing business expenses under final regs An important development this year will affect every business, including yours. The IRS has...